I’ve traveled to approximately 20 countries. Initially, I would use currency exchange kiosks as many as four or so times in each country. Eventually, I realized that I was unnecessarily throwing money away in currency exchange fees. I learned that my credit card(s) offered much more competitive exchange fees (if charging any at all).

The little kiosks have much higher per transaction overhead costs. My advice: stick to the kiosks for only converting enough money for public transportation or some other small amount; use your credit card everywhere else. You’ll likely save money in the long run.

The wife and I are leaving for our move to Tennessee within the next 3 hrs (2060 miles to go).

Friday, March 31, 2006

Thursday, March 30, 2006

Frugal Yet Romantic Ideas for You and Your Mate

First off, this post is not directly related to finance. However, it can be useful to you financially, especially if you want a few frugal yet romantic ideas, or you simply want to stimulate an existing relationship/marriage.

Ideas are taken from a brochure that I kept from my early college years titled “101 Ways to Eroticize Safer Sex.” The brochure was handed out by my Alma Mater’s peer health advocates group.

56 of the 101 ways to eroticize safer sex were excluded because they were either specific to the area of the University or not as tame/clean as what I’d like to post on this blog. Listed, in no particular order:

(1) Dance together in your room

(2) Go horseback riding

(3) Comb each other’s hair

(4) Play Frisbee

(5) Give flowers for no specific reason

(6) Take a hot air balloon ride

(7) Go to a music festival

(8) Hang out at a bookstore or music store

(9) Play board games

(10) Kiss each other slowly

(11) Take a sauna together

(12) Wear each other’s boxers

(13) Build sand castles

(14) Finger paint each other

(15) Take a nap together

(16) Give Eskimo or butterfly kisses

(17) Go hiking together

(18) Play wrestle

(19) Share a lollipop

(20) Give each other a foot and hand massage

(21) Listen to each other’s heart beat

(22) Watch the sun rise/sunset

(23) Leave a rose on your mate’s windshield

(24) Bring your mate breakfast in bed

(25) Drink a cappuccino at an outdoor café

(26) Read Shakespearean sonnets

(27) Go to an aquarium or zoo

(28) Take a carriage ride

(29) Play putt-putt golf

(30) Go dancing

(31) Go bowling

(32) Make bread together

(33) Cook a candle light dinner together

(34) Go kite flying

(35) Stay overnight in a bed and breakfast

(36) Rollerblade together

(37) Take a stroll in the rain

(38) Surprise your mate with a bouquet of balloons

(39) Take a walking tour of area attractions

(40) Swing on a porch

(41) Go bicycling together

(42) Leave each other love notes

(43) Swing in a hammock

(44) Sip hot chocolate w/ marshmallows by the fireplace

(45) Flirt with one another

Ideas are taken from a brochure that I kept from my early college years titled “101 Ways to Eroticize Safer Sex.” The brochure was handed out by my Alma Mater’s peer health advocates group.

56 of the 101 ways to eroticize safer sex were excluded because they were either specific to the area of the University or not as tame/clean as what I’d like to post on this blog. Listed, in no particular order:

(1) Dance together in your room

(2) Go horseback riding

(3) Comb each other’s hair

(4) Play Frisbee

(5) Give flowers for no specific reason

(6) Take a hot air balloon ride

(7) Go to a music festival

(8) Hang out at a bookstore or music store

(9) Play board games

(10) Kiss each other slowly

(11) Take a sauna together

(12) Wear each other’s boxers

(13) Build sand castles

(14) Finger paint each other

(15) Take a nap together

(16) Give Eskimo or butterfly kisses

(17) Go hiking together

(18) Play wrestle

(19) Share a lollipop

(20) Give each other a foot and hand massage

(21) Listen to each other’s heart beat

(22) Watch the sun rise/sunset

(23) Leave a rose on your mate’s windshield

(24) Bring your mate breakfast in bed

(25) Drink a cappuccino at an outdoor café

(26) Read Shakespearean sonnets

(27) Go to an aquarium or zoo

(28) Take a carriage ride

(29) Play putt-putt golf

(30) Go dancing

(31) Go bowling

(32) Make bread together

(33) Cook a candle light dinner together

(34) Go kite flying

(35) Stay overnight in a bed and breakfast

(36) Rollerblade together

(37) Take a stroll in the rain

(38) Surprise your mate with a bouquet of balloons

(39) Take a walking tour of area attractions

(40) Swing on a porch

(41) Go bicycling together

(42) Leave each other love notes

(43) Swing in a hammock

(44) Sip hot chocolate w/ marshmallows by the fireplace

(45) Flirt with one another

Wednesday, March 29, 2006

Some of The Best Coupons are at the Post Office

I've moved alot in my life. About 50% of the time I find great coupons in the USPS address change packages. But wait, you don't have to fill the forms out in pen anymore. You can now go to USPS.com and get both the form and the coupons.

Here's the coupons I found:

10% off at Home Depot

Free Direct TV (intro period)

15% off at JCPenney

Here's the coupons I found:

10% off at Home Depot

Free Direct TV (intro period)

15% off at JCPenney

Tuesday, March 28, 2006

My Master’s Thesis on Perceived Financial Conditions is approved!!

I just got the last signature on my Master's Thesis on "Perceived Financial Conditions."

Thesis is specific to enlisted personnel in the U.S. Navy. People classified their financial situation as either: (1) In over head; (2) Tough to make ends meet; (3) Occasional difficulties; (4) Makes ends meet w/o much difficulty; (5) Comfortable and secure.

I separately modeled perceived financial conditions (PFCs) of single and married personnel to determine how various demographic and attitudinal characteristics affect PFC levels. Many of the results can be applied to most anybody.

I’ll start posting more stuff on this in future.

Thesis is specific to enlisted personnel in the U.S. Navy. People classified their financial situation as either: (1) In over head; (2) Tough to make ends meet; (3) Occasional difficulties; (4) Makes ends meet w/o much difficulty; (5) Comfortable and secure.

I separately modeled perceived financial conditions (PFCs) of single and married personnel to determine how various demographic and attitudinal characteristics affect PFC levels. Many of the results can be applied to most anybody.

I’ll start posting more stuff on this in future.

Sunday, March 26, 2006

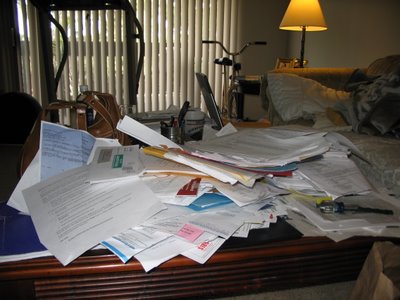

It's a Shredding Weekend

Here's a picture of what we have ahead of us today. The wife and I are going through all our paperwork and class notes and having a shredding weekend. We're moving this Friday from Monterey, CA to Memphis, TN. We're just getting our paperwork in order prior to the movers getting here on Tues and Wed. So far we've discarded/shredded four full bags worth of documents. Here's a picture of "some" of the victims (papers) we'll have fun (LOL) going through today.

This ignores our filing cabinet, which might also get some attention. One of the half-full bags of shredded documents:

This ignores our filing cabinet, which might also get some attention. One of the half-full bags of shredded documents:

What is Your Pension or Annuity Worth?

Many of you may want to either “juice-up” your net worth statements, or simply know what your pension is worth today, assuming your company remains solvent. Others may want to know what a fixed benefit annuity is worth.

John at ourmoneymatters blog posed the question: How do I determine the present value of my pension, if I retired today? He stated that he would collect $525/month starting today and be able to collect this amount for life. I posted an initial solution on his site that was wrong (ran numbers around 1am PST, bit tired I guess). Here’s how to figure out the value of a pension (Method #1 using simple calculator, Method #2 using a finance calculator).

I assumed a personal discount rate (rate of expected return) of 0.5% per month and a life expectancy of 30 years (360 months) past-retirement date.

1. Using a simple calculator with an exponential “^” function (minimum requirement)

(a) Determine present value of an annuity. Using the formula

PV annuity = [ 1 – (1 + R)^-n] (P/R)

R = interest rate in decimal form

P= payment

N= number of periods

Filling in numbers you get:

PV annuity = [ 1 – (1 + 0.005)^-360] (525/0.005)

PV annuity = [ 1 – 0.166] (105,000)

PV annuity = $87,570

Slight round of error, exact answer would be $87,565.60

2. Using a financial calculator like TI BAII

This is a two step five value problem.

Step 1:

a) Assuming a 6% discount rate (6%/12 months = 0.5%/month)

b) Assuming 30yr life expectancy

N= 360 months

I/Y= 0.5%/month

PV= $0

PMT= $525/month

FV= ?

Plugging into financial calculator, you get a future value of $527,370.40. Now working backwards in step 2:

N= 360 months

I/Y = 0.5%/month

PV= ?

PMT= $0/month

FV= $527,370.40

Solving for PV you get $87,565.60.

Your present value (PV) will be smaller if you expect a rate of return higher than 6% on investments. These calculations are exactly the same for annuities too.

Friday, March 24, 2006

Making Money in a Housing Bubble: S&P Launching Tradable Real Estate Indexes

Today's S&P announced the launching of 10 indexes that "will track housing prices in various regions of the

The 10 separate "city-based" indexes will track: Boston, Chicago, Denver, Las Vegas, Los Angeles, Miami, New York Commuter Index, San Diego, San Francisco and Washington D.C. (source: S&P)

These indexes will essentially allow people to go short or long real estate.

Here's an article that provides some additional details.

Thursday, March 23, 2006

Ebay's PayPal Goes Mobile (New Text Message Format for Utilizing PayPal)

Hot off the press! Heard on NPR this morning about PayPal's new text messaging form of payment. Surfed the web and here's a couple of articles on it.

Article 1

Article 2

By the way, I just turned in all 5 chapters of my Master's Thesis on "Perceived Financial Conditions." We'll see how the editing goes. It's 540am here in Cali and I haven't yet been asleep. I'm jacked up on chocolate covered espresso beans right now. Wonder when it'll wear off.

Article 1

Article 2

By the way, I just turned in all 5 chapters of my Master's Thesis on "Perceived Financial Conditions." We'll see how the editing goes. It's 540am here in Cali and I haven't yet been asleep. I'm jacked up on chocolate covered espresso beans right now. Wonder when it'll wear off.

Wednesday, March 22, 2006

How I Got a Free Starbucks Drink Today

Ok, I didn't get it today, but the barista gave me a coupon for any free drink next time. This is how it went down. I ordered my favorite drink in a non-standard format:

Venti, Mocha Frap Light w/ Whip Cream. The Whip Cream is normally not included.

The barista took my order, failed to write "whip cream" on my cup and handed the order over to the actual barista making the drinks. As you can expect, the barista making the drink didn't put the whip cream on until well after trying to give it to me (I had to ask a 2nd time).

The barista making the drink said that they'd put it on if I only asked at purchase. Well, I did ask. However, I kept my mouth shut and walked out... The barista that actually took my order noticed this and chased me down to give me a coupon for one free drink (anything).

I guess it's one of their policies to compensate you if they don't write the right thing on your cup, or otherwise mess up...

I've ordered the same drink about 100 times and they've forgotten the whip cream about 5 times. This is the first time that I got a coupon out of it. I guess, I am usually in a hurry, so much so that they would never be able to catch up with me...Or, the people taking my order previously were never paying attention.

Oh, there might be one other reason they did this. A manager was conducting job interviews outside for new baristas. Maybe, they wanted to ensure that the interviewer didn't overhear any complaints.

Perhaps they would have given me the coupon those other 5 times if I only asked. You might be able to use this info next time they mess up your order. Perhaps they'll hook you up with a free-drink coupon too.

Venti, Mocha Frap Light w/ Whip Cream. The Whip Cream is normally not included.

The barista took my order, failed to write "whip cream" on my cup and handed the order over to the actual barista making the drinks. As you can expect, the barista making the drink didn't put the whip cream on until well after trying to give it to me (I had to ask a 2nd time).

The barista making the drink said that they'd put it on if I only asked at purchase. Well, I did ask. However, I kept my mouth shut and walked out... The barista that actually took my order noticed this and chased me down to give me a coupon for one free drink (anything).

I guess it's one of their policies to compensate you if they don't write the right thing on your cup, or otherwise mess up...

I've ordered the same drink about 100 times and they've forgotten the whip cream about 5 times. This is the first time that I got a coupon out of it. I guess, I am usually in a hurry, so much so that they would never be able to catch up with me...Or, the people taking my order previously were never paying attention.

Oh, there might be one other reason they did this. A manager was conducting job interviews outside for new baristas. Maybe, they wanted to ensure that the interviewer didn't overhear any complaints.

Perhaps they would have given me the coupon those other 5 times if I only asked. You might be able to use this info next time they mess up your order. Perhaps they'll hook you up with a free-drink coupon too.

Are You Wealthy Enough? Equation for Determining If You're as Wealthy as You Should Be

I really love the Stanley/Danko series of "The Millionaire Next Door" and "The Millionaire Mind." Both authors provide a useful equation for people to determine if they're wealthy relative to their income.

Equation (From: page 13, "The Millionaire Next Door"): "Multiply your age times your realized pretax annual household income from all sources except inheritances. Divide by ten. This, less any inherited wealth, is what your net worth should be."

I forget where they mention it, but people that exceed this are considered "prodigious accumulators of wealth." While, I believe passive income is a more powerful indicator than actual wealth, I continue to use the above equation as our running benchmark for wealth.

Use of the above equation for my wife and I yields a required net worth of $400,934.60. While we're not there yet, we'll get caught up with this variable benchmark within the next 5 years. Kind of hard since I started over after a divorce in early 2003, and the wife was also starting, financially, from a low point.

Equation (From: page 13, "The Millionaire Next Door"): "Multiply your age times your realized pretax annual household income from all sources except inheritances. Divide by ten. This, less any inherited wealth, is what your net worth should be."

I forget where they mention it, but people that exceed this are considered "prodigious accumulators of wealth." While, I believe passive income is a more powerful indicator than actual wealth, I continue to use the above equation as our running benchmark for wealth.

Use of the above equation for my wife and I yields a required net worth of $400,934.60. While we're not there yet, we'll get caught up with this variable benchmark within the next 5 years. Kind of hard since I started over after a divorce in early 2003, and the wife was also starting, financially, from a low point.

Stock Market Correction of 10% or More: Neil Cavuto Hosted Guy With 80% Accuracy Track Record

Ok, don't laugh. I'm more of a person who identifies with fundamentals. However, I was watching Neil Cavuto last night when he had a gentleman by the name of Henry Weingarten on. Neil said that this guy had an 80% accuracy track record for predicting the markets.

Mr. Weingarten runs the Astrology Fund. Couldn't find a ticker symbol for this. It seems more like it's an investing newsletter. Mr. Weingarten predicted, last night, that a stock market correction of 10% or more will occur within 90 days of March 29, 2006.

The astrologer noted a looming debt-dollar crisis. The gentleman's website is a bit hokey; however, I was able to deduce that he feels that the Nasdaq is the index that is most likely to fall.

I don't mean to be a chicken little here. I'm only trying to report an interesting/entertaining story. Here's the guy's website.

Here's some of the astrologer's commentary on the stock market.

Here's the markets that this astrologer favors.

Tuesday, March 21, 2006

6% Dividend Stock + Opinion/Use of Google Finance Worked In

Goggle Finance (Beta) debuted today with a yawn... While the Goggle quote screen provides more info than the initial Yahoo Finance quote, it's more cluttered. The Yahoo Finance quote is cleaner (in my opinion) and provides far more options in it's left side tool bar.

Here's the two of them used for my favorite high yield dividend stock (15% tax rate) :

Google finance CTCO quote

Yahoo finance CTCO quote

Here's an S&P / Busineweek article on the company. Morningstar also ranks this company "5 Stars." If you look at its cash on the books, you'll see that it has more than double it's annual dividend in cash and is also in a positive cash flow position. Last year, I believe, it gave a special dividend of $12.

I have never bought stock in a tele-communications company. However, this one seems to have enough DSL growth to offset it's declining land-line usage, and it has enough barriers to competitor entry b/c of the unique region it serves.

I have not yet bought shares, but I am seriously considering buying shares within the next 10 days.

Here's the two of them used for my favorite high yield dividend stock (15% tax rate) :

Google finance CTCO quote

Yahoo finance CTCO quote

Here's an S&P / Busineweek article on the company. Morningstar also ranks this company "5 Stars." If you look at its cash on the books, you'll see that it has more than double it's annual dividend in cash and is also in a positive cash flow position. Last year, I believe, it gave a special dividend of $12.

I have never bought stock in a tele-communications company. However, this one seems to have enough DSL growth to offset it's declining land-line usage, and it has enough barriers to competitor entry b/c of the unique region it serves.

I have not yet bought shares, but I am seriously considering buying shares within the next 10 days.

Plan on Retiring Early? How to Withdraw Funds From Retirement Accounts Without 10% Penalty

Here's a way in which you can withdraw funds from your retirement accounts before 59 1/2. Simply convert them to an IRA and take the minimum distribution for at least 5 years.

More details can be found here.

Also, you can find more details in a shorter article in this month's Money magazine.

More details can be found here.

Also, you can find more details in a shorter article in this month's Money magazine.

Monday, March 20, 2006

My Next Stock/ETF Trade

I'm planning on rolling my profits from the New York Stock Exchange (NYX) shares into one or more of the following:

Citigroup (C)

Vanguard Financials ETF (VFH)

IShares Germany (EWG)

IShares Canada (EWC)

IShares Australia (EWA)

Reasons:

(1) Financials since FED is nearing end of rate tightening cycle, bodes well for profit margins.

(2) Canada & Australia as trickle down plays on natural resources.

(3) Germany based on own opinion that German Labor Practicies will evolve to be more competitive with the global economy. Plus, this European country has a huge supply of human/intellectual capital that could be leveraged for remarkable benefits... Especially if they had longer work weeks!

Opinions?

Citigroup (C)

Vanguard Financials ETF (VFH)

IShares Germany (EWG)

IShares Canada (EWC)

IShares Australia (EWA)

Reasons:

(1) Financials since FED is nearing end of rate tightening cycle, bodes well for profit margins.

(2) Canada & Australia as trickle down plays on natural resources.

(3) Germany based on own opinion that German Labor Practicies will evolve to be more competitive with the global economy. Plus, this European country has a huge supply of human/intellectual capital that could be leveraged for remarkable benefits... Especially if they had longer work weeks!

Opinions?

Maserati GranSport Giveaway By CNBC Squawk Box

Long-shot odds, but you can win a Maserati GranSport from CNBC by participating in the "Squawk Box Fantasy Portfolio Challenge."

Registration: NOW OPEN

Competition starts: 4 Apr 2006

Competition ends: 26 May 2006

Winner Announced: 31 May 2006

MY DAILY SQUAWK BOX FANTASY PORTFOLIO ANSWERS (SEE COMMENTS SECTION)

1st Place: Maserati GranSport, CNBC also pays your taxes on it

2nd Place: 25 2nd place prices, prize not yet announced

How it works:

(1) Start off with $1 million in Squawk Box trading money

(2) Can add $5,000 each day to your portfolio by answering Squawk Box trivia question about that day's 830-900 EST segment.

(3) Person with highest total portfolio after stock trading and answering Squawk Box trivia questions wins car.

Registration for competition here.

Other competition details can be obtained here.

Other information about car can be obtained here.

Registration: NOW OPEN

Competition starts: 4 Apr 2006

Competition ends: 26 May 2006

Winner Announced: 31 May 2006

MY DAILY SQUAWK BOX FANTASY PORTFOLIO ANSWERS (SEE COMMENTS SECTION)

1st Place: Maserati GranSport, CNBC also pays your taxes on it

2nd Place: 25 2nd place prices, prize not yet announced

How it works:

(1) Start off with $1 million in Squawk Box trading money

(2) Can add $5,000 each day to your portfolio by answering Squawk Box trivia question about that day's 830-900 EST segment.

(3) Person with highest total portfolio after stock trading and answering Squawk Box trivia questions wins car.

Registration for competition here.

Other competition details can be obtained here.

Other information about car can be obtained here.

amerivest

http://infoweb.newsbank.com/iw-search/we/InfoWeb?p_action=doc&p_docid=1107504E938B20C8&p_docnum=7&p_queryname=2&p_product=NewsBank&p_theme=aggregated4&p_nbid=D64S53DPMTE0Mjg1NDY3OS44MDc1MTU6MTo1OnVzbjY3

Advantages of exchange-traded funds include generally (though not always) lower annual operating expenses and fewer taxable distributions. With ETFs you have more choices to slice a portfolio by tracking narrower market sectors, such as stocks from a particular industry or country. (Narrow indexes, however, can increase risk and defeat the purpose of broad diversification.)

Arguably, the biggest drawback of ETFs is that you pay brokerage commissions every time you buy or sell. With no-load mutual funds there are no such commissions.

For investors with big portfolios ETF commissions can be more than offset by the lower operating costs and tax savings. But for small investors who want to add regularly to their accounts, such as putting in $100 or $200 every month, commissions can be a significant expense.

In addition, commissions can discourage investors from the recommended risk-reducing practice of "rebalancing," or buying or selling components of a portfolio periodically to keep its asset allocation to the intended mix.

Now, however, under a program offered by Amerivest, an online investment advisory service and subsidiary of TD Ameritrade Holding Corp., investors can buy, sell and rebalance diversified ETF portfolios with no commissions, although they must pay an annual advisory fee.

I find the Amerivest concept worthy of mention, just as I occasionally write about other financial products and services. As always, I am not recommending anything, just bringing the program to your attention.

Personally, I feel confident putting together a diversified low-cost portfolio and would not pay an ongoing fee for advice. For investors who need guidance, however, I find the Amerivest fee reasonable, considering the waiving of commissions and the broadly diversified, low-expense portfolios the service recommends. Even do-it-yourselfers can peek at the free Amerivest Web site, www.amerivest.com, and obtain ideas from the sample portfolios.

The Amerivest advisory fee is 0.35 percent of assets a year on accounts of $100,000 or more; 0.50 percent on accounts between $20,000 and $99,999, and the lesser of 2.95 percent or $100 a year on accounts under $20,000.

One-fourth of the fee is deducted each quarter.

"What we offer is a disciplined portfolio strategy geared for the long term," said Joe Moglia, chief executive of TD Ameritrade, the name of the combined brokerage from Ameritrade's acquisition of TD Waterhouse.

Although not the same as the more detailed guidance you could receive from a financial planner whom you would meet face to face, "if you are comfortable with the Internet, this is something you can do," Moglia said.

----------

Humberto Cruz is a columnist for Tribune Media Services. E-mail him at yourmoney@tribune.com.

- - -

How one program works

Under a program offered by Amerivest, investors can buy, sell and rebalance diversified ETF portfolios with no commissions. Basically, it works like this:

You go online and answer questions about your financial goals, risk tolerance, investment time frame and amount available to invest. Based on your answers, Amerivest, which is part of a registered investment advisory firm, will suggest one of more than two dozen portfolios built largely on ETFs representing a mix of asset classes designed to balance potential risk and return.

For example, one sample $50,000 "balanced" portfolio consists of 50 percent equities, including U.S. large-cap, U.S. small-cap and international stocks, including those from emerging markets; 49 percent fixed income from short-term and intermediate-term U.S. government bonds, and 1 percent cash.

You are free to accept or modify the recommendation--the service bills itself as your "financial co-pilot," meaning you remain in charge.

For example, while you'll be reminded to assess progress toward your goals, it's your job to reassess those goals and your risk tolerance periodically to make sure the portfolio remains right for you.

"The investor needs to take responsibility for himself," said Joe Moglia, chief executive of TD Ameritrade. "If his goals have changed, if his risk tolerance has changed, nobody knows that better than the individual."

You can buy ETFs online without paying commission

Chicago Tribune (IL)

March 19, 2006

Author: Humberto Cruz, a columnist for Tribune Media Services

March 19, 2006

Author: Humberto Cruz, a columnist for Tribune Media Services

Estimated printed pages: 3

Many financial advisers who favor low-cost, broadly diversified and tax-efficient portfolios for wealthy clients are switching from no-load index mutual funds to exchange-traded funds, or at least including ETFs in the portfolios. Now, an online brokerage that caters to do-it-yourselfers is pitching exchange-traded funds to individual investors, along with advice on how to use them.

Both ETFs and index mutual funds seek to match the performance of a market benchmark, some as broad as the overall U.S. stock or bond market, while keeping costs low. One key difference is that ETFs trade like a stock on a stock exchange. You can buy or sell them at any time during the trading day at the current price and place "limit" orders to specify how much you are willing to pay or accept.

Advantages of exchange-traded funds include generally (though not always) lower annual operating expenses and fewer taxable distributions. With ETFs you have more choices to slice a portfolio by tracking narrower market sectors, such as stocks from a particular industry or country. (Narrow indexes, however, can increase risk and defeat the purpose of broad diversification.)

Arguably, the biggest drawback of ETFs is that you pay brokerage commissions every time you buy or sell. With no-load mutual funds there are no such commissions.

For investors with big portfolios ETF commissions can be more than offset by the lower operating costs and tax savings. But for small investors who want to add regularly to their accounts, such as putting in $100 or $200 every month, commissions can be a significant expense.

In addition, commissions can discourage investors from the recommended risk-reducing practice of "rebalancing," or buying or selling components of a portfolio periodically to keep its asset allocation to the intended mix.

Now, however, under a program offered by Amerivest, an online investment advisory service and subsidiary of TD Ameritrade Holding Corp., investors can buy, sell and rebalance diversified ETF portfolios with no commissions, although they must pay an annual advisory fee.

I find the Amerivest concept worthy of mention, just as I occasionally write about other financial products and services. As always, I am not recommending anything, just bringing the program to your attention.

Personally, I feel confident putting together a diversified low-cost portfolio and would not pay an ongoing fee for advice. For investors who need guidance, however, I find the Amerivest fee reasonable, considering the waiving of commissions and the broadly diversified, low-expense portfolios the service recommends. Even do-it-yourselfers can peek at the free Amerivest Web site, www.amerivest.com, and obtain ideas from the sample portfolios.

The Amerivest advisory fee is 0.35 percent of assets a year on accounts of $100,000 or more; 0.50 percent on accounts between $20,000 and $99,999, and the lesser of 2.95 percent or $100 a year on accounts under $20,000.

One-fourth of the fee is deducted each quarter.

"What we offer is a disciplined portfolio strategy geared for the long term," said Joe Moglia, chief executive of TD Ameritrade, the name of the combined brokerage from Ameritrade's acquisition of TD Waterhouse.

Although not the same as the more detailed guidance you could receive from a financial planner whom you would meet face to face, "if you are comfortable with the Internet, this is something you can do," Moglia said.

----------

Humberto Cruz is a columnist for Tribune Media Services. E-mail him at yourmoney@tribune.com.

- - -

How one program works

Under a program offered by Amerivest, investors can buy, sell and rebalance diversified ETF portfolios with no commissions. Basically, it works like this:

You go online and answer questions about your financial goals, risk tolerance, investment time frame and amount available to invest. Based on your answers, Amerivest, which is part of a registered investment advisory firm, will suggest one of more than two dozen portfolios built largely on ETFs representing a mix of asset classes designed to balance potential risk and return.

For example, one sample $50,000 "balanced" portfolio consists of 50 percent equities, including U.S. large-cap, U.S. small-cap and international stocks, including those from emerging markets; 49 percent fixed income from short-term and intermediate-term U.S. government bonds, and 1 percent cash.

You are free to accept or modify the recommendation--the service bills itself as your "financial co-pilot," meaning you remain in charge.

For example, while you'll be reminded to assess progress toward your goals, it's your job to reassess those goals and your risk tolerance periodically to make sure the portfolio remains right for you.

"The investor needs to take responsibility for himself," said Joe Moglia, chief executive of TD Ameritrade. "If his goals have changed, if his risk tolerance has changed, nobody knows that better than the individual."

Sunday, March 19, 2006

An Expensive Way to Get A Free 4 GB IPOD Nano

If you want a free 4GB IPOD Nano and you're looking for a new discount broker, look here.

I don't have the spare change, but I'm considering opening a TD Waterhouse account just to buy my favorite municipal bond fund: NHMRX

You'll need to deposit $50k to qualify for the IPOD Nano. However, my favorite municipal bond fund only requires $3,000 for initial investment.

I don't have the spare change, but I'm considering opening a TD Waterhouse account just to buy my favorite municipal bond fund: NHMRX

You'll need to deposit $50k to qualify for the IPOD Nano. However, my favorite municipal bond fund only requires $3,000 for initial investment.

Saturday, March 18, 2006

Two Steps to Take Now to Avoid Bouncing Checks in the Future

Besides having more money, the following are two tips that will help you avoid bouncing checks in the future.

(1) Ensure all of your personal accounts at the bank are linked. I was personally a victim of this with Navy Federal Credit Union (NFCU). A few years ago, I had my money in a NFCU money market account collecting the highest possible yield. I wrote a check for an amount well less than the funds that I had between my accounts only to find out that the accounts were not linked together. After bouncing this check, I asked if my checking account could be linked with my other account and was told NO!

My other bank does this. It routinely will tap a savings account in the event the checking account balance is insufficient. While your results may vary, I highly recommend you ask your teller or customer service representative if linking accounts is possible.

(2) Apply for a line of credit and have that line of credit attached to your checking account. I do this with all of my bank accounts now. In the event your checking account has insufficient funds, funds will be debited from your line of credit. Lines of credit typically run between 10 - 12%. You don't get charged anything if you don't use it. However, short term use in exceptional circumstances can be far cheaper than bouncing a check.

(1) Ensure all of your personal accounts at the bank are linked. I was personally a victim of this with Navy Federal Credit Union (NFCU). A few years ago, I had my money in a NFCU money market account collecting the highest possible yield. I wrote a check for an amount well less than the funds that I had between my accounts only to find out that the accounts were not linked together. After bouncing this check, I asked if my checking account could be linked with my other account and was told NO!

My other bank does this. It routinely will tap a savings account in the event the checking account balance is insufficient. While your results may vary, I highly recommend you ask your teller or customer service representative if linking accounts is possible.

(2) Apply for a line of credit and have that line of credit attached to your checking account. I do this with all of my bank accounts now. In the event your checking account has insufficient funds, funds will be debited from your line of credit. Lines of credit typically run between 10 - 12%. You don't get charged anything if you don't use it. However, short term use in exceptional circumstances can be far cheaper than bouncing a check.

Friday, March 17, 2006

What $218K will Buy You in Suburbs of Memphis

House bought for $218k at end of Feb in one of the suburbs just outside of Memphis in Shelby county, Tennesse.

House is 3100 sq ft, not including the 3 car garage.

House is 3100 sq ft, not including the 3 car garage.

Thursday, March 16, 2006

Took Profits in my Shares of New York Stock Exchange (Position Was Up 55% Since November Purchase)

I sold 35% of my NYX shares today at $89/share. My cost basis on this was $57.11. Thus, I was up 55.8% or 53+% when you factor in sharebuilder.com's obscene cost for limit orders.

I bought shares in Archipeligo in November and have enjoyed the ride ever since (especially after the AX share conversion to NYX shares). I sold because the velocity of it's share price gains is hitting a road block between $88 and $90. Plus, in the short term, there's the possibility that it'll over-pay in a bidding war for the London Stock Exchange. There's a chance that NYX will announce plans for a conversion to a fully electronic exchange. That will cause shares to rocket higher; however, while shareholders prefer this, I doubt very seriously they'll announce this within the next six months.

Selling 35% of my shares today took an amount of money off the table equivalent to my profits made to date. I'll have to marinate over the market these next few days to see where i'll put the money next. I doubt very seriously that NYX will drop below $80 anytime soon. It's a great stock; however, my position had grown much higher than all my others. Just want to do some more diversifying, and I want to try and find a different stock that will appreciate like NYX already did.

I bought shares in Archipeligo in November and have enjoyed the ride ever since (especially after the AX share conversion to NYX shares). I sold because the velocity of it's share price gains is hitting a road block between $88 and $90. Plus, in the short term, there's the possibility that it'll over-pay in a bidding war for the London Stock Exchange. There's a chance that NYX will announce plans for a conversion to a fully electronic exchange. That will cause shares to rocket higher; however, while shareholders prefer this, I doubt very seriously they'll announce this within the next six months.

Selling 35% of my shares today took an amount of money off the table equivalent to my profits made to date. I'll have to marinate over the market these next few days to see where i'll put the money next. I doubt very seriously that NYX will drop below $80 anytime soon. It's a great stock; however, my position had grown much higher than all my others. Just want to do some more diversifying, and I want to try and find a different stock that will appreciate like NYX already did.

Wednesday, March 15, 2006

New FDIC limits on retirement accounts go into effect next month

I previously wrote up the fact that higher FDIC limits on retirement accounts will go into effect no later than 1 Nov. Federal Deposit Insurance Corporation (FDIC) has finalized interim rules for higher FDIC limits much earlier than the time previously allotted it.

Effective 1 Apr 2006, retirement accounts will be covered up to $200k. Unable to attach specific article. However it's called: "Higher FDIC limit on retirement accounts begins April 1" and is available via google news.

The article is rather long but informative.

Effective 1 Apr 2006, retirement accounts will be covered up to $200k. Unable to attach specific article. However it's called: "Higher FDIC limit on retirement accounts begins April 1" and is available via google news.

The article is rather long but informative.

Emigrant Direct Account Disclosure You're Required to Accept

When setting up your account w/ Emigrant Direct, make sure you check the "Account Disclosure" section. Then check out the "refusal to permit withdrawal" subsection.

In this section it specifically states that: "The Bank chooses to exercise its legal rights to require up to 60 days' advance written notice of any intended withdrawal from this Account and the 60 days have not passed since we received the required notice from you."

I've never seen this associated with any other checking or savings account. I went to another popular site, ING Direct, and didn't find a similar disclosure (during a quick site review).

Please post a remark here if you're familiar with this clause at any of these other online banks, or if you had problems withdrawing funds because of this clause.

I went ahead and opened an Emigrant Direct account; however, I'm a bit leery of putting more than 5% of my assets in an account that has this clause.

In this section it specifically states that: "The Bank chooses to exercise its legal rights to require up to 60 days' advance written notice of any intended withdrawal from this Account and the 60 days have not passed since we received the required notice from you."

I've never seen this associated with any other checking or savings account. I went to another popular site, ING Direct, and didn't find a similar disclosure (during a quick site review).

Please post a remark here if you're familiar with this clause at any of these other online banks, or if you had problems withdrawing funds because of this clause.

I went ahead and opened an Emigrant Direct account; however, I'm a bit leery of putting more than 5% of my assets in an account that has this clause.

Tuesday, March 14, 2006

My Favorite Real Estate Magazine for Identifying Trends and Location Characteristics

I go to Borders Books about once every two weeks for reading magazines and books for free. I was disappointed this weekend when they didn't have my favorite real estate magazine in stock.

It's not a "real estate" magazine as you may be thinking. The magazine is called "Where-To-Retire." Puzzled at why a 31 year old is looking in the retirement section?

Ha, Ha, anybody that follows trends should take a moment to look at the magazine. This particular magazine caters to a huge demographic group that is entering a period where many are likely to up-root and retire to new locations fueling area specific booms. Yes, there's a housing bubble; however, if you follow the retirement dollars, look for the good deals and diversify your areas, you may do better than your friends that are only buying houses in one area.

Don't get me wrong, buying houses in only one area allows you to self manage the properties. However, if there's a serious earthquake, series of tornados or a hurricane, your real estate empire might take a larger hit than necessary.

The magazine I mentioned above will help you identify trends and area characteristics that may be favorable to you. Each magazine covers several communities with well thought out articles and discusses characteristics such as:

Median Housing Price

City/Town Profile

Arts & Cultural Activities

Recreation & Outdoor Activities

Continuing Education Opportunities

Hospital

Airports

Tax Info

Climate & Weather

At the end of the articles, key characteristics are bulleted in a quick read section. Occasionally, they will write up some communities that are only for seniors, but these types of articles are limited.

Anyways, the magazine gives you plenty of ideas so that you can judge whether or not the area is of any interest...Then, you can just go to yahoo real estate (or other site) and start surfing to find your next investment property. Ultimately, you might live there. If not, you know that many others in the baby boomer demographic are reading the same magazine and making real estate decisions based in part from the magazine or from peers that might read the magazine.

Monday, March 13, 2006

How to Pilfer the 529 College Savings Plan for Cruise Line Trip(s) Without Tax Penalty

Have you been saving laboriously in a 529 plan? What if your intended beneficiary gets a scholarship? How can you pilfer the funds without tax penalty and spend them on yourself in retirement? I'll specifically address using 529 plans for pseudo-cruise line trips after a giving you my opinion and brief subject overview.

I'm not a proponent of 529 plans, unless you've already met your retirement savings goals; however, they do serve a purpose. I hope you know that contributions can be made to 529 plans even if you don't have children. In this case, it would be presumed that you would be the one using the money to go to school. You're always suppose to be learning so this is somewhat plausible.

Non-taxable 529 Plan disbursements can be made not only for tuition but room and board expenses at the local school, even if you don't live and eat on campus. You simply have to take a course load that's 1/2 full time. In some Junior Colleges and distance learning programs 1/2 full time is as little as 4 credit hours.

Ok, now to subject of this posting, there are college programs at sea that are on cruise liners and include numerous recreational ports of call. Consider the following program if you want a legitimate way of pilfering the 529 plan and concurrently going on an extended cruise line trip:

Semester at Sea <- This program is associated with

Read this for a write up on general college at sea programs. Generally, this strategy is good only if you want to take an extended vacation (likely in retirement years) and don't mind taking a couple of classes.

Sunday, March 12, 2006

Lexus 5% / 1.5% Points Back Credit Card

This card is useful for not only those that own a Lexus but also those planning on buying one... It also has a feature for doubling your points to a 10% equivalent when buying or leasing a new Lexus. I frown on the limitation to only new. I would like to see it include purchase of pre-owned vehicles. Nonetheless, the card is still useful.

I typically take our cars to the regular quick-lube or Wal-Mart for oil changes. However, I take our cars to the dealership at roughly 30k mile intervals. I just got back from our local Lexus dealership and found a visa card offer attached to the bill. The details of the offer are below.

This credit card gives 5% back on all Lexus dealership transactions and 1.5% back on purchases elsewhere. The % back is in the form of points that can be redeemed in a number of ways, principally at the dealership. Dealerships are inherently expensive for maintenance; however, if you're like me and bring it to the dealership for only major service appointments (30k, 60k, 90k, 120k, etc), then this might be a prudent option.

There is no cap on the points that accrue. There is a 50k point transaction cap on down payments made with it (equivalent to $10k down payment).

I didn't bother checking out the APR. I don't believe in using a credit card unless you can pay it off or you're using their money at 3% or less APR.

Details can be found at: Lexus Pursuits Visa

I typically take our cars to the regular quick-lube or Wal-Mart for oil changes. However, I take our cars to the dealership at roughly 30k mile intervals. I just got back from our local Lexus dealership and found a visa card offer attached to the bill. The details of the offer are below.

This credit card gives 5% back on all Lexus dealership transactions and 1.5% back on purchases elsewhere. The % back is in the form of points that can be redeemed in a number of ways, principally at the dealership. Dealerships are inherently expensive for maintenance; however, if you're like me and bring it to the dealership for only major service appointments (30k, 60k, 90k, 120k, etc), then this might be a prudent option.

There is no cap on the points that accrue. There is a 50k point transaction cap on down payments made with it (equivalent to $10k down payment).

I didn't bother checking out the APR. I don't believe in using a credit card unless you can pay it off or you're using their money at 3% or less APR.

Details can be found at: Lexus Pursuits Visa

Short Term Savings Goal of $40k to Buy Real Estate

We've got a short term savings goal of $40k for a 20+% down payment. Ideally, we'd want the money by July 31st. However, we would probably be able to come up with only $30k by then. The other $10k would come from a short term loan from our ROTH IRAs, a signature loan or HELOC. Ideally, I would prefer not to do any of these. However, we're concurrently maxing out our 401Ks & IRAs and it's tough doing both. We shouldn't have to pilfer the IRA accounts or take loans if we defer the purchase past October 1st (ideally, this is preferred).

We're planning on real estate in either central

a) Condo on

b) Areas surrounding

c) Areas surrounding Bentonville (Wal-Mart country). This would require less than $40k for 20% down payment.

We'd be able to manage property in

As for

The Condo on the

Saturday, March 11, 2006

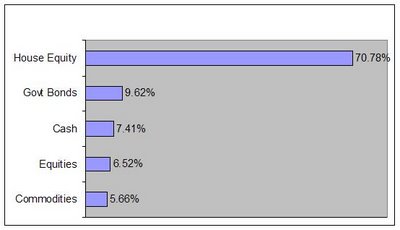

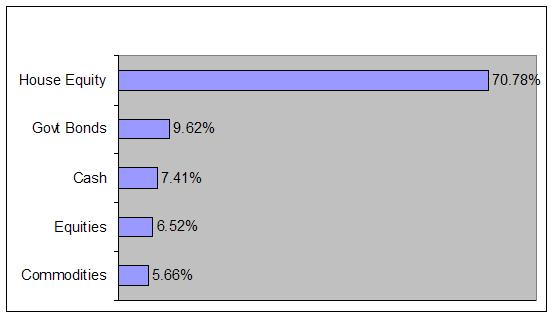

Here’s a Graphical Picture and Discussion of our Household Investments

Here's our distribution of investment assets. As I said in my intro, we save aggressively and invest moderately. The house equity represents three houses. The government bonds are collecting about 4.7+%. I'm essentially waiting for a market correction before I increase our position in equities. Commodities is a bit of a misnomer. The following components make up our position in "commodities:"

a) BHP Billiton (BHP)

b) Rio Tinto (RTP)

c) Natural Resources Fund (UMESX)

d) Deutche Bank Commodities (DBC)

e) Pimco Commodies (PCRDX)

f) Gold (GLD)

I'm a bit heavy into commodities because I believe inflation will continue to be a problem. I view the yield curve as an indicator for inflation. In my opinion, the dip or inversion in the yield curve represents a short term decrease in our rate of inflation. However, in my opinion, this short term decrease is just that SHORT TERM.

I'm a bit heavy into commodities because I believe inflation will continue to be a problem. I view the yield curve as an indicator for inflation. In my opinion, the dip or inversion in the yield curve represents a short term decrease in our rate of inflation. However, in my opinion, this short term decrease is just that SHORT TERM.

a) BHP Billiton (BHP)

b) Rio Tinto (RTP)

c) Natural Resources Fund (UMESX)

d) Deutche Bank Commodities (DBC)

e) Pimco Commodies (PCRDX)

f) Gold (GLD)

I'm a bit heavy into commodities because I believe inflation will continue to be a problem. I view the yield curve as an indicator for inflation. In my opinion, the dip or inversion in the yield curve represents a short term decrease in our rate of inflation. However, in my opinion, this short term decrease is just that SHORT TERM.

I'm a bit heavy into commodities because I believe inflation will continue to be a problem. I view the yield curve as an indicator for inflation. In my opinion, the dip or inversion in the yield curve represents a short term decrease in our rate of inflation. However, in my opinion, this short term decrease is just that SHORT TERM.Friday, March 10, 2006

Is an Education Worth the Expense?

Outside the improvements in self esteem, communication and analytical skills, an education boils down to return on investment. I risk making this post as exciting as a "Wonder Years Ben Stein Lecture," but here goes...

Do you think it will make you more competitive for promotions? Do you think that a new career field or higher education would give you enough of a marginal increase in salary to merit the time spent?

I'm a proponent of education. However, you must understand that it's important to monetize the worth of an education. You don't want to enroll in graduate programs online blindly thinking you'll get a pay raise. Here's some things to consider:

1. How much of a pay cut will you sustain over the period of pursuing an education? If you don't experience a salary decrease, do you think that your focus on an after hours education will impede your focus at work, thereby limiting promotion opportunities?

2. Once you graduate from a program, do you think you'll take a pay cut until you establish some form of seniority?

3. How long will you work in the new career field and benefit from the improved education?

The best thing to do, strictly from a monetary since, is to:

a) Monetize the net increase in salary that you expect over the remainder of your career: Present Value[ (new salary - prior salary)*(Number years remaining in work force)].

b) Monetize any impacts (decreases) to your annual salary while going to school

c) Monetize the cost of your psychic energy expended on school work. Could you have otherwise spent your psychic energy (brain power) teaching your children something useful or otherwise contribute to the household? This cost may be ignored, but you should be aware of it.

Now determine the net present value of a, b and c.

Example... If you make $90k/yr now and you pay $125k to go to med school and increase your salary to $200k/yr for a 15yr career as an M.D.

Benefit "A": ($200k - $90k) for 15 years @ 5% discount rate, Pay Raise Deferred Six Years From Now = $852,000.67

Cost "B": Lose $90/yr salary for six years @ 5% discount rate = -$456,812.29 (present value of unearned income b/c in Med School/Residency)

Cost "C": Ignored, but could be considered

Net Present Value of "A, B, C" = $852,000.67 - $456,812.29 = $395,188.38

Now determine your return on education: Return on education: [(Net Present Value A,B,C) – Education Cost]/Education Cost * 100 = ($395,188.38 - $125,000)/($125,000) * 100 = 216% return

Got a headache from all this? Don’t know how to determine Net Present Values (NPVs)? Don’t know how to use the five major keys of a financial calculator? I can try to help via email. If there’s a lot of questions, I’ll post some lessons on the blog.

It’s important to note that I simplified the discussion and calculations some for the sake of saving space.

By the way, I’m going to make some changes to this blog over the next two weeks to make the layout a bit more efficient.

Do you think it will make you more competitive for promotions? Do you think that a new career field or higher education would give you enough of a marginal increase in salary to merit the time spent?

I'm a proponent of education. However, you must understand that it's important to monetize the worth of an education. You don't want to enroll in graduate programs online blindly thinking you'll get a pay raise. Here's some things to consider:

1. How much of a pay cut will you sustain over the period of pursuing an education? If you don't experience a salary decrease, do you think that your focus on an after hours education will impede your focus at work, thereby limiting promotion opportunities?

2. Once you graduate from a program, do you think you'll take a pay cut until you establish some form of seniority?

3. How long will you work in the new career field and benefit from the improved education?

The best thing to do, strictly from a monetary since, is to:

a) Monetize the net increase in salary that you expect over the remainder of your career: Present Value[ (new salary - prior salary)*(Number years remaining in work force)].

b) Monetize any impacts (decreases) to your annual salary while going to school

c) Monetize the cost of your psychic energy expended on school work. Could you have otherwise spent your psychic energy (brain power) teaching your children something useful or otherwise contribute to the household? This cost may be ignored, but you should be aware of it.

Now determine the net present value of a, b and c.

Example... If you make $90k/yr now and you pay $125k to go to med school and increase your salary to $200k/yr for a 15yr career as an M.D.

Benefit "A": ($200k - $90k) for 15 years @ 5% discount rate, Pay Raise Deferred Six Years From Now = $852,000.67

Cost "B": Lose $90/yr salary for six years @ 5% discount rate = -$456,812.29 (present value of unearned income b/c in Med School/Residency)

Cost "C": Ignored, but could be considered

Net Present Value of "A, B, C" = $852,000.67 - $456,812.29 = $395,188.38

Now determine your return on education: Return on education: [(Net Present Value A,B,C) – Education Cost]/Education Cost * 100 = ($395,188.38 - $125,000)/($125,000) * 100 = 216% return

Got a headache from all this? Don’t know how to determine Net Present Values (NPVs)? Don’t know how to use the five major keys of a financial calculator? I can try to help via email. If there’s a lot of questions, I’ll post some lessons on the blog.

It’s important to note that I simplified the discussion and calculations some for the sake of saving space.

By the way, I’m going to make some changes to this blog over the next two weeks to make the layout a bit more efficient.

Thursday, March 09, 2006

When are You Justified In Buying a New/Like-New Car?

In an age of instant credit, negative savings rates and instant gratification, I ask when are you justified in buying a new/like-new car?

Joseph White wrote and article published in the Feb 28th Wall Street Journal’s Personal Finance section. It's titled "Cars Last Longer, Driving a Shift In All Aspects of the Auto Sector." It states that average service lives of vehicles (based on 2001 government data) are:

a) Cars: 13 years, 152k miles

b) Light Trucks (sport utilities, vans, trucks): 14 years, 180k miles

We have two 1998 model cars. One with 112k (Lexus) and mine with 121k (Acura). I'm trying to hold off on splurging. I'll probably wait till we exceed either the 13yr or 152k mile mark, then it's reasonable for us to buy a new/like-new car. The last car we had was a 1990 Celica GTS and was sold at 144.5k miles.

Cars are really the only thing I'm materialistic about. Oh, and the Lexus was bought used. Yeah, I'm ignoring the fact that some imports typically have longer than average service lives. Please be kind if you slam me for not being frugal enough.

Opinions?

Joseph White wrote and article published in the Feb 28th Wall Street Journal’s Personal Finance section. It's titled "Cars Last Longer, Driving a Shift In All Aspects of the Auto Sector." It states that average service lives of vehicles (based on 2001 government data) are:

a) Cars: 13 years, 152k miles

b) Light Trucks (sport utilities, vans, trucks): 14 years, 180k miles

We have two 1998 model cars. One with 112k (Lexus) and mine with 121k (Acura). I'm trying to hold off on splurging. I'll probably wait till we exceed either the 13yr or 152k mile mark, then it's reasonable for us to buy a new/like-new car. The last car we had was a 1990 Celica GTS and was sold at 144.5k miles.

Cars are really the only thing I'm materialistic about. Oh, and the Lexus was bought used. Yeah, I'm ignoring the fact that some imports typically have longer than average service lives. Please be kind if you slam me for not being frugal enough.

Opinions?

Wednesday, March 08, 2006

GO New York Stock Exchange (NYX)!!! Stock Cheerleading With a Couple Insightful Comments about NYX

I'm so excited that my position in Archipelago (AX) has been so profitable recently, especially today. I made two purchases in mid to late November with a net cost of $57.11/share (stock closed at $80 today). The conversion of AX to NYX caused the shares to spike 24% today. That 24% spike tells me: 1) A hybrid stock exchange is only a speed bump in the path of complete conversion to a fully electronic stock exchange. Yes, the float (# shares trading) on this stock is small, but 24% today!!! I might just sell 33% of my NYX shares into strength here (by Friday) and take a little off the table.

I heard an interesting tidbit on NPR while coming in to school. The New York Stock Exchange could operate at 10% of its current operating cost if it converts to a fully electronic trading system. I sincerely hope none of my readers work on the floor of the stock exchange.

I will get around to detailing my stock portfolio with a nice picture, diagram or spreadsheet by Sunday night. Please remember, I said in my intro that I save aggressively and invest moderately. NYX has certainly offset the short term hit I’ve taken in my commodities position... I will likely include a discussion on the inverted yield and how it ties to some of my portfolio decisions (sounds exciting... HA, HA, sarcasm)

I'm not a rocket-scientist or anything with stock picks. I've been typically good with identifying companies with sound strategies. I have been poor with timing sales of shares. Cases in point: I was buying shares of Ameritrade in the high eights and low nines within last 22 months. I was also buying SanDisk and Garmin around this time frame. These were roughly 3 of 10 stocks I was buying... The other stocks didn't tank or anything, well, one did (EBAY)... I just cashed out about a month or so before their rallies to set up a savings account for house down payment.

Hopefully, talking though my investment decisions on here will help me better rationalize my choices. More to come later, .getting back to thesis on Perceived Financial Conditions…

I heard an interesting tidbit on NPR while coming in to school. The New York Stock Exchange could operate at 10% of its current operating cost if it converts to a fully electronic trading system. I sincerely hope none of my readers work on the floor of the stock exchange.

I will get around to detailing my stock portfolio with a nice picture, diagram or spreadsheet by Sunday night. Please remember, I said in my intro that I save aggressively and invest moderately. NYX has certainly offset the short term hit I’ve taken in my commodities position... I will likely include a discussion on the inverted yield and how it ties to some of my portfolio decisions (sounds exciting... HA, HA, sarcasm)

I'm not a rocket-scientist or anything with stock picks. I've been typically good with identifying companies with sound strategies. I have been poor with timing sales of shares. Cases in point: I was buying shares of Ameritrade in the high eights and low nines within last 22 months. I was also buying SanDisk and Garmin around this time frame. These were roughly 3 of 10 stocks I was buying... The other stocks didn't tank or anything, well, one did (EBAY)... I just cashed out about a month or so before their rallies to set up a savings account for house down payment.

Hopefully, talking though my investment decisions on here will help me better rationalize my choices. More to come later, .getting back to thesis on Perceived Financial Conditions…

My Counter Prosper.com Interest/Dividend Strategy

First of all, I love the idea of applying Reverse-Dutch Auctions to the loan process. I applaud Prosper and may, in the near future, allocate up to $2000 towards some Prosper.com investments. I want to give it some time though to learn from the successes and failures of others using Prosper. I do have some strategies that I will post in the near future that may help you with diversifying your Prosper loans. I will also form and post the name of my counter-intuitive Prosper group name.

Right now, I'm specifically interested in buying preferred stock in companies. I ran a search this morning and found 70 companies with dividend rates above 8%. I have not yet found a companion website that does yield-to-maturity calculations though. I'm going to hold off buying any of these preferred stocks until I can blog on here an easy-to-use site for determining yields-to-maturity. If not, I’ll probably show the required calculation and give a tutorial. Of the list of 70 preferred stocks, there were a few that caught my eye. I feel that buying a few preferred stocks could diversify your investments and hedge your risks against default on any Prosper loans.

I do have one problem with Prosper right now. It appears from the reporting of other blogs that there is an excessive period where PROSPER is collecting interest on your money without sharing this interest (let me know if I’m wrong). This idea is inherently flawed in that it increases the likelihood of lenders increasing their risk tolerance and lending to higher risk candidates just to get their net preferred yield on loans.

Here’s Wikipedia’s definition of yield-to-maturity. They define YTM for only bonds; however, I believe that an equivalent calculation could be done for preferred stocks. If not exact, a close enough SWAG. R/ FJ

Right now, I'm specifically interested in buying preferred stock in companies. I ran a search this morning and found 70 companies with dividend rates above 8%. I have not yet found a companion website that does yield-to-maturity calculations though. I'm going to hold off buying any of these preferred stocks until I can blog on here an easy-to-use site for determining yields-to-maturity. If not, I’ll probably show the required calculation and give a tutorial. Of the list of 70 preferred stocks, there were a few that caught my eye. I feel that buying a few preferred stocks could diversify your investments and hedge your risks against default on any Prosper loans.

I do have one problem with Prosper right now. It appears from the reporting of other blogs that there is an excessive period where PROSPER is collecting interest on your money without sharing this interest (let me know if I’m wrong). This idea is inherently flawed in that it increases the likelihood of lenders increasing their risk tolerance and lending to higher risk candidates just to get their net preferred yield on loans.

Here’s Wikipedia’s definition of yield-to-maturity. They define YTM for only bonds; however, I believe that an equivalent calculation could be done for preferred stocks. If not exact, a close enough SWAG. R/ FJ

Is Google Adsense a Crock of _____ ?

After a significant amount of hard work and $10 in earned advertisement revenue, google disabled my account and refused disbursement of my earnings.

It seems they don’t want you to screen the advertisements placed on your website. Each day over the past week I clicked on advertisements that I was unfamiliar with and blocked those that I didn’t like at Adsense’s block competitor list. Apparently it’s MY MISTAKE for trying to screen chaff that their filter lets through. They apparently classified this as fraudulent clicks.

To add insult to injury, GOOGLE doesn’t give you a 1-800 number to call to rectify the matter.

I’ll make every attempt to retrieve my list of “blocked competitor adds” and share them with you. Frankly, I was disappointed that the Adsense Algorithm allows so much crappy advertisement through. If this isn’t resolved soon, I’ll drop my favorite search engine in favor of Yahoo. Any comments/tips?

It seems they don’t want you to screen the advertisements placed on your website. Each day over the past week I clicked on advertisements that I was unfamiliar with and blocked those that I didn’t like at Adsense’s block competitor list. Apparently it’s MY MISTAKE for trying to screen chaff that their filter lets through. They apparently classified this as fraudulent clicks.

To add insult to injury, GOOGLE doesn’t give you a 1-800 number to call to rectify the matter.

I’ll make every attempt to retrieve my list of “blocked competitor adds” and share them with you. Frankly, I was disappointed that the Adsense Algorithm allows so much crappy advertisement through. If this isn’t resolved soon, I’ll drop my favorite search engine in favor of Yahoo. Any comments/tips?

Free Money: My Opinion on 0% APR Credit Card Offers

Ok, I risk making waves amongst the 0% APR chasers. However, I’ll make my opinions known.

My background: At the age of twenty-five, I had never looked at my FICO score, but I had a credit representative tell me it was the highest they had ever seen. Forty-two months later I had been married and divorced. My FICO score was now in the mid five-hundreds. Eighteen or slightly more months later the FICO score was back up to mid-7s. Now it's 771. It took a slight hit and fell from 780s surrounding my recent home purchase.

I believe first in keeping the number of inquiries on your credit report to a low number. Right now I have seven unique inquiries in the last two years. Credit lenders typically look at any series of inquiries occurring within a 15 day period as related and count them as one unique inquiry (I’m reasonably confident on the number of days, but correct me if I’m wrong).

If I get my inquiries below 7, perhaps around 5, I’ll probably get the HSBC 1% rebate MasterCard with a one year 0% APR. Once the one year promotional APR is over, I’d switch back to my 5% and 2% rebate credit cards. It's important to note that you must exercise a reasonable amount of due diligence to find a credit card that doesn't charge a 3% balance transfer fee. The HSBC MasterCard is not one of those. If you need one of those, the Discover miles card might do this for you. Anyways, I generally hate BALANCE TRANSFERS because they only prolong the inevitable (facing reality and paying it off). Only those that set up parallel high yield savings account(s), avoid hurting themselves to bad; however, their FICO score still suffers a bit.

Other credit card tidbits:

a) You're FICO score is partially determined by your "credit card available balance percentage." If you have a credit card with a zero balance and close it, both your FICO score and percentage will get worse.

b) If you close a credit card account anyways, it's best to close those accounts that have the shortest history. If you want to close an account that has been open a long time, it's generally best to close those accounts used the least (relative to your other accounts used over this longer period of time).

I extend my apologies to my subscribers. I have submitted this story several times today. However, it wasn’t picked up on one of the pfblog aggregators properly. I’m resubmitting “fresh” copies until it goes though. Hopefully, this bug (on my end or there’s) will be worked out today and not persist beyond this posting.

My background: At the age of twenty-five, I had never looked at my FICO score, but I had a credit representative tell me it was the highest they had ever seen. Forty-two months later I had been married and divorced. My FICO score was now in the mid five-hundreds. Eighteen or slightly more months later the FICO score was back up to mid-7s. Now it's 771. It took a slight hit and fell from 780s surrounding my recent home purchase.

I believe first in keeping the number of inquiries on your credit report to a low number. Right now I have seven unique inquiries in the last two years. Credit lenders typically look at any series of inquiries occurring within a 15 day period as related and count them as one unique inquiry (I’m reasonably confident on the number of days, but correct me if I’m wrong).

If I get my inquiries below 7, perhaps around 5, I’ll probably get the HSBC 1% rebate MasterCard with a one year 0% APR. Once the one year promotional APR is over, I’d switch back to my 5% and 2% rebate credit cards. It's important to note that you must exercise a reasonable amount of due diligence to find a credit card that doesn't charge a 3% balance transfer fee. The HSBC MasterCard is not one of those. If you need one of those, the Discover miles card might do this for you. Anyways, I generally hate BALANCE TRANSFERS because they only prolong the inevitable (facing reality and paying it off). Only those that set up parallel high yield savings account(s), avoid hurting themselves to bad; however, their FICO score still suffers a bit.

Other credit card tidbits:

a) You're FICO score is partially determined by your "credit card available balance percentage." If you have a credit card with a zero balance and close it, both your FICO score and percentage will get worse.

b) If you close a credit card account anyways, it's best to close those accounts that have the shortest history. If you want to close an account that has been open a long time, it's generally best to close those accounts used the least (relative to your other accounts used over this longer period of time).

I extend my apologies to my subscribers. I have submitted this story several times today. However, it wasn’t picked up on one of the pfblog aggregators properly. I’m resubmitting “fresh” copies until it goes though. Hopefully, this bug (on my end or there’s) will be worked out today and not persist beyond this posting.

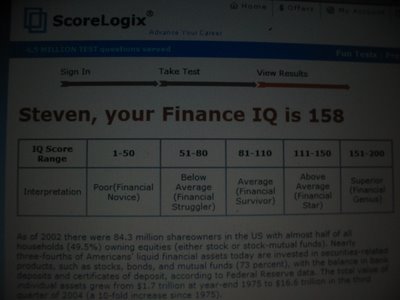

My Financial IQ Per SCORELOGIX.COM

Ok, I took the Finance IQ exam at scorelogix. I took it once, seriously, and had them send the results to my hotmail account. My mistake. I never received it. Took it again without reading the questions and going by memory... Hotmail screwed up receipt again. Took it a third time without reading the questions and answering by memory, but had score sent to gmail account. Gmail classified the score report as "spam." If you take this, you'll want to be careful receiving the exam results.

The exam was taken unaided (without any references), only a calculator for one question. The exam is eight pages with approximately five questions per page. The picture will enlarge if you click on it. It says: "Steven Your Finance IQ is 158"

The scoring breakout is:

1-50: Poor Financial Novice

51-80: Below Average (Financial Struggler)

81-110: Average (Financial Survivor)

111-150: Above Average (Financial Star)

151-200: Superior (Financial Genius)

I'll update my score and picture if the results from my first test ever get transmitted to my hotmail account. You can access scorelogix here.

The exam was taken unaided (without any references), only a calculator for one question. The exam is eight pages with approximately five questions per page. The picture will enlarge if you click on it. It says: "Steven Your Finance IQ is 158"

The scoring breakout is:

1-50: Poor Financial Novice

51-80: Below Average (Financial Struggler)

81-110: Average (Financial Survivor)

111-150: Above Average (Financial Star)

151-200: Superior (Financial Genius)

I'll update my score and picture if the results from my first test ever get transmitted to my hotmail account. You can access scorelogix here.

Tuesday, March 07, 2006

Non-Finance Entry: Another Way for Sports Fans to Ruin Your Productivity at Work & Home

It is becoming increasingly more important for sports media contracts to include the right to broadcast both television and internet content. CBS has finally addressed this and will be offering March Madness basketball events over the internet.

Here's their blurb: "NCAA® March Madness™ on Demand is totally FREE for the first time ever! Get LIVE game broadcasts of CBS Sports television coverage of NCAA® March Madness™ streaming on your broadband-connected computer.

All 56 games from the first three rounds of the tournament will be available FREE.* Plus, watch highlights and recaps all the way through the championship!"

To register, go here.

This sports news post will be removed after one week to help maintain personal finance relevance.

Here's their blurb: "NCAA® March Madness™ on Demand is totally FREE for the first time ever! Get LIVE game broadcasts of CBS Sports television coverage of NCAA® March Madness™ streaming on your broadband-connected computer.

All 56 games from the first three rounds of the tournament will be available FREE.* Plus, watch highlights and recaps all the way through the championship!"

To register, go here.

This sports news post will be removed after one week to help maintain personal finance relevance.

Recommend You Read This Guy's Blog

If you want to be heard at a well respected site, read the entries and post comments here. Dr Rutledge has been a money manager for one or more presidents and appears frequently on CNBC and FOX. He is also associated with Rutledge Capital.

The Rutledge Capital website has a very efficient lay-out. It reminds me of the Wall Street Journal in that it has key topics in column format for very quick read and overall website survey.

It's important to understand how he thinks. One of his key points involves Leonardo da Vinci: "When people asked Leonardo da Vinci the secret of his creative and inventing genius, he replied "Saper Vedere," to know how to see. Our objective is to help people see the link between government policy, capital formation, and growth, then help them see strategies for growing their businesses, increasing the value of their investments, and improving their economic lives."

Other descriptive comments about how he thinks are listed here.

I know the U.S. has an attitude about the Fed Chairman... When the Fed Chairman speaks, everybody listens. I listen to Dr. Rutledge as closely as most other people listen to the Fed.

Where do I find time for this??? It puzzles me too, I'm a full time student till the end of March... At the end of April I start a full time job. I'll start drafting blog entries at night then... Fingers crossed that chapters IV and V of my thesis will turn out fine (working on over these next 10 days)...

Later, FJ

The Rutledge Capital website has a very efficient lay-out. It reminds me of the Wall Street Journal in that it has key topics in column format for very quick read and overall website survey.

It's important to understand how he thinks. One of his key points involves Leonardo da Vinci: "When people asked Leonardo da Vinci the secret of his creative and inventing genius, he replied "Saper Vedere," to know how to see. Our objective is to help people see the link between government policy, capital formation, and growth, then help them see strategies for growing their businesses, increasing the value of their investments, and improving their economic lives."

Other descriptive comments about how he thinks are listed here.

I know the U.S. has an attitude about the Fed Chairman... When the Fed Chairman speaks, everybody listens. I listen to Dr. Rutledge as closely as most other people listen to the Fed.